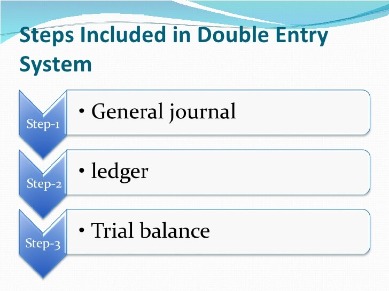

Bookkeeping

New PPP Loan Amount Calculations for Schedule C Filers

Therefore, any questions or concerns regarding individual PPP loan applications must be directed to your lender. The amount of any refinanced EIDL used what can you do if a customer doesnt pay an invoice for will be included in the calculation of “payroll costs.” An applicant may use this form only if the applicant files an IRS Form 1040, Schedule C, and uses gross income to calculate PPP loan amount. Note that one of the certifications requires you to certify that if this application is for a Second Draw loan, you must have used all First Draw PPP loan amounts on eligible expenses prior to disbursement of the Second Draw PPP Loan. To fill out the application, we find it easier not to start at the beginning.

Full-Time Equivalency (FTE) Reduction Calculation

Unfortunately, many sole proprietors have already applied for PPP loan funding, rendering this new change useless to them. With only a couple of days left in this latest PPP financing round, it’s not likely to make a significant impact unless the deadline is extended and Schedule C filers are allowed to resubmit to maximize their loan amounts. Lenders typically decide when to submit individual PPP loan applications to SBA.

First Draw Loan If You Have Employees

Under section 206(c) of the Taxpayer Certainty and Disaster Tax Relief Act of 2020, an employer that is eligible for the employee retention credit (ERC) can claim the ERC even if the employer has received a Small Business Interruption Loan under the Paycheck Protection Program (PPP). The eligible employer can claim the ERC on any qualified wages that are not counted as payroll costs in obtaining PPP loan forgiveness. Any wages that could count toward eligibility for the ERC or PPP loan forgiveness can be applied to either of these two programs, but not both. No, the amount of loan forgiveness requested for nonpayroll costs may not include any amount attributable to the business operation of a tenant or sub-tenant of the PPP borrower or, for home-based businesses, household expenses. The examples below (directly from the SBA guidance) illustrate this rule.

- Now that the calculations in the worksheets are completed, you should be able to fill out the rest of the application.

- Payroll costs generally are incurred on the day the employee’s pay is earned (i.e., on the day the employee worked).

- The SBA’s recent Interim Final Rule (IFR) states that Schedule C filers (that’s you, sole proprietors) can now use gross income instead of net to calculate PPP loan amounts.

Another term you’ll see throughout the application is “FTE,” which stands for Full-time Equivalent or Full-time Equivalency. Filling out your PPP forgiveness application will receipts by wave on the app store be very different depending on whether you have employees or not. There is a lot to digest here and hopefully it will make sense once you approach it methodically. In this article, we provide both background information as well as details on specific questions related to the application when that information is available in official guidance. A small amount of interest may have accrued in the meantime and, if so, you’ll need to also pay that. If you keep the loan, the guidance suggests you should still spend those funds for authorized purposes.

Am I an employee?

PPP is a loan designed to provide a direct incentive for small businesses to keep their workers on payroll. (ii) the average total monthly payment for employee payroll costs incurred or paid by the borrower during the same year elected by the borrower; by (2) 2.5 (or, only for a borrower assigned a NAICS code beginning with 72 at the time of disbursement; or (B) $2,000,000. The most complicated part of filling out the forgiveness application is filling out the payroll sections. We’ll provide general information here but you may have questions unique to your situation. (It’s 62 pages long but there is a table of contents starting on page 9 that may help you find an answer more quickly.) Also keep in mind this information does not replace professional accounting or legal advice.

Who may qualify

The IFR states that it applies to “loans approved after the effective date. Enter high low method calculate variable cost per unit and fixed cost the amount of business mortgage interest payments during the covered period for any business mortgage obligation on real or personal property incurred before February 15, 2020. Enter the Borrower’s total average weekly full-time equivalency (FTE) during the chosen reference period.

If using 2020 to calculate loan amount, this is required regardless of whether you have filed a 2020 tax return with the IRS. You must provide a 2020 invoice, bank statement, or book of record to establish you were in operation on or around February 15, 2020. Enter the total amount paid by the borrower for employer state and local taxes assessed on employee compensation (e.g., state unemployment insurance tax); do not list any taxes withheld from employee earnings. Make sure you understand that you have these options for calculating FTE. This calculation is going to be very important for forgiveness purposes as you’ll see when we walk through the application.

Individuals with income from self-employment from 2019 for which they can file a 2019 Form 1040 Schedule C cannot consider expenses incurred between January 1, 2020 and February 14, 2020. Once the loan has been disbursed and the lender has filed Form 1502 with the SBA, there is no option to reapply for a larger amount. The world’s first financial health suite that streamlines access to the best financing options. Compare your top small business financing options, from over 160 financial products – with Nav.

Check the box if the Borrower, together with its affiliates (to the extent required under SBA’s interim final rule on affiliates (85 FR (April 15, 2020)) and not waived under 15 U.S.C. 636(a)(36)(D)(iv)), received PPP loans with an original principal amount in excess of $2 million. If you received more than $2 million (with or without affiliates) make sure you review this with your advisors. Enter the total number of employees at the time of the Borrower’s PPP Loan Application. If you received more than one disbursement, use the date of the first one. As you follow along here, note that we have copied actual fields and their instructions from the SBA application.

“Forgiveness is capped at 2.5 months’ worth (2.5/12) of an owner-employee or self employed individual’s 2019 or 2020 compensation (up to a maximum $20,833 per individual in total across all businesses). The individual’s total compensation may not exceed $100,000 on an annualized basis, as prorated for the period during which the payments are made or the obligation to make the payments is incurred. For borrowers that elect to use a ten-week covered period, the cap is ten weeks’ worth (10/52) of 2019 or 2020 compensation (approximately 19.23 percent) or $19,231 per individual, whichever is less, in total across all businesses. For a covered period longer than 2.5 months, the amount of loan forgiveness requested for owner-employees and self-employed individuals’ payroll compensation is capped at 2.5 months’ worth (2.5/12) of 2019 or 2020 compensation (up to $20,833) in total across all businesses. In general, payroll costs paid or incurred during the covered period are eligible for forgiveness. (More details of payroll expenses paid vs. incurred are listed in the FAQs below.) Salary, wages, or commission payments to furloughed employees, bonuses or hazard pay during the covered period may be eligible for forgiveness, provided they don’t exceed the $100,000 annual cap.